How Much College Really Costs in 2026: Sticker Price vs. Net Price

Average tuition and total cost of attendance for 2025–26, why most families never pay the sticker price, and how to estimate what you'll actually pay.

The number on a college's website and the number a family actually pays are usually very different. Confusing the two is how students rule out schools they could afford — and fall in love with schools they can't. This guide walks through what college costs in 2026, why the published price is closer to a hotel rack rate than a real price, and how to estimate your own number before you apply anywhere.

The 2025–26 numbers

The College Board's Trends in College Pricing is the standard reference for published prices. For the 2025–26 academic year, average published tuition and fees for full-time undergraduates:

| Institution type | Tuition & fees | Total cost of attendance* |

|---|---|---|

| Public two-year (in-district) | $4,150 | — |

| Public four-year (in-state) | $11,950 | $29,910 |

| Public four-year (out-of-state) | $31,880 | $49,080 |

| Private nonprofit four-year | $45,000 | $62,570 |

*Total cost of attendance includes tuition, fees, housing, food, books, and personal expenses for on-campus students.

Two things jump out. First, tuition is often less than half the real bill — at an in-state public, housing and food cost more than tuition itself. Second, the sticker gap between public and private looks enormous ($11,950 vs. $45,000), but as you'll see below, the net gap is often much smaller.

Prices also vary wildly by state: in-state tuition at public four-years ranges from around $6,400 in Florida to over $18,000 in Vermont and New Hampshire.

Cost of attendance: the number that actually matters

Every school publishes a cost of attendance (COA) — the full annual budget:

- Tuition and fees — the academic charges

- Housing and food — on-campus room and board, or an off-campus estimate

- Books and supplies — increasingly bundled digitally

- Transportation and personal expenses — travel home, laundry, phone, everything else

COA matters for two reasons: it's the realistic annual budget you should plan against, and it's the ceiling on your total financial aid. When comparing schools, always compare COA to COA — never one school's tuition to another school's full budget.

Sticker price vs. net price

Net price = cost of attendance − grants and scholarships (money you never repay). It's what your family actually covers through savings, income, and loans.

Most families don't pay sticker. The majority of full-time students receive grant aid, and at many private colleges the average discount off published tuition is more than half. That produces the counterintuitive result every family should internalize:

A $45,000 private school that gives you a $25,000 grant costs less than a $31,900 out-of-state public that gives you nothing. Never rule a school in or out on sticker price alone.

Where grant money comes from

- Need-based aid — determined by the FAFSA (and at a few hundred mostly private colleges, the CSS Profile). Federal Pell Grants top out at $7,395 for 2026–27; the bigger need-based money is usually the college's own institutional grants.

- Merit aid — awarded for grades and scores, often automatically. State flagships and mid-tier privates use merit scholarships aggressively to recruit; the most selective schools generally offer none (their aid is entirely need-based).

- State programs — many states fund substantial grants for in-state students (Georgia's HOPE, Florida's Bright Futures, and similar), usually with their own deadlines and GPA requirements.

How to estimate your net price before applying

Every college is federally required to publish a net price calculator — search "[school name] net price calculator" or find it linked from the financial aid office. Enter your family's income and assets and you get an estimate of grants and net cost. It takes about ten minutes per school.

Rules of thumb when you run them:

- Run the calculator for every school on your list — before you fall in love, and definitely before applying anywhere Early Decision.

- Treat the result as ±a few thousand dollars, closer for straightforward finances (W-2 income, no business or divorce complications).

- Recheck if your finances change — a job change or a sibling entering college can move the number substantially.

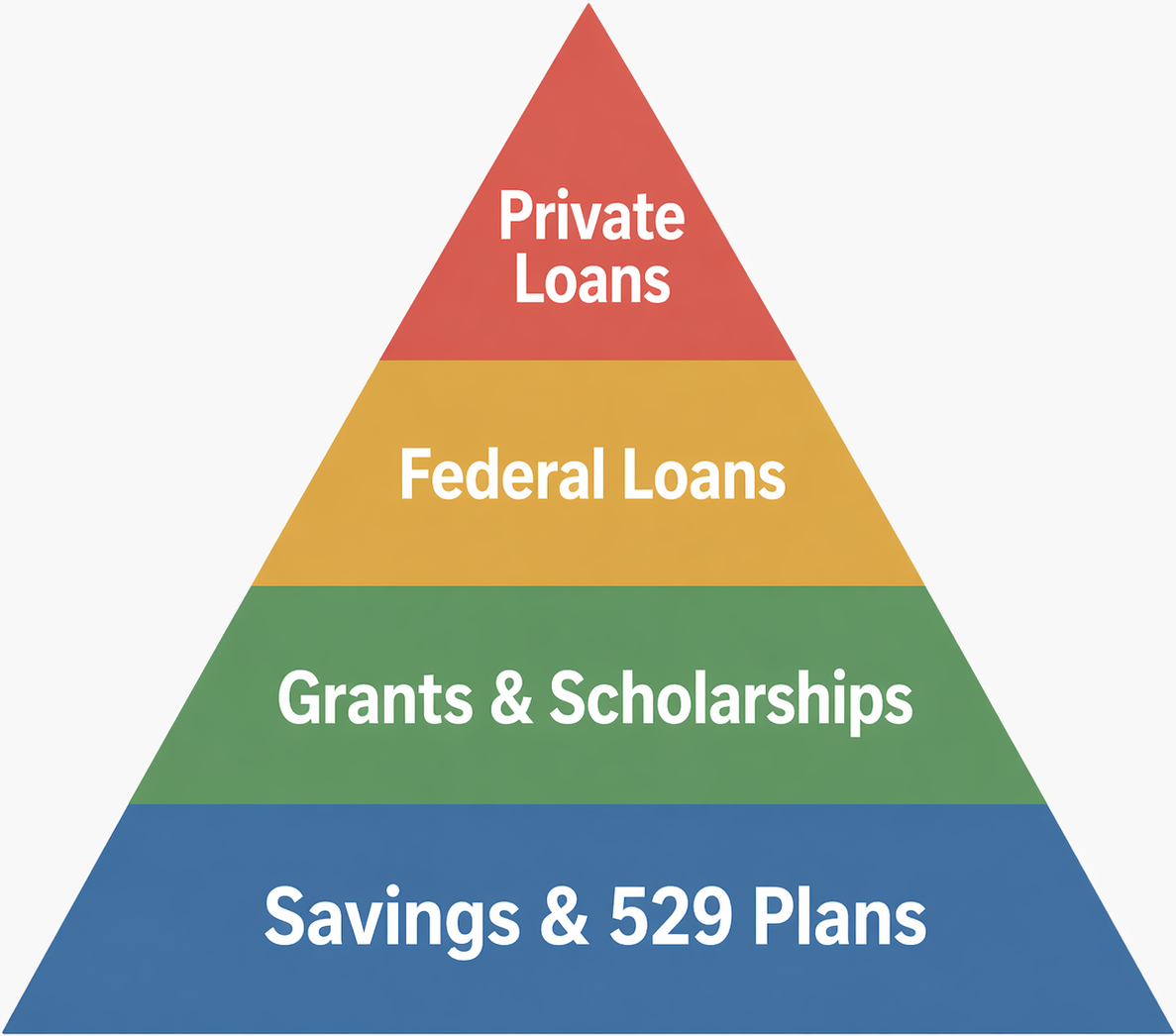

Paying for the rest: the pecking order

Once grants are applied, families cover the remaining net price. The order matters, because the sources range from free to expensive:

- Savings and 529 plans — money that costs nothing to use.

- Grants and scholarships — beyond college aid, outside scholarships from employers, community groups, and national competitions stack on top.

- Work-study and part-time work — a campus job in the $2,000–$4,000-per-year range is manageable alongside classes.

- Federal student loans — fixed rates, income-driven repayment options, no cosigner. Dependent freshmen can borrow up to $5,500 in Direct Loans (rising modestly each year after). That cap is a feature: roughly $27,000 of federal debt across four years is a manageable outcome for most graduates.

- Private loans and parent borrowing — the expensive top of the pyramid. If a school requires large private loans or parent debt to close the gap, that's the strongest signal the school doesn't fit financially.

Four-year cost, not one-year cost

Two final multipliers that change the real total:

- Graduation rate. A school where students routinely take five or six years costs 25–50% more than its COA suggests. Four-year graduation rates are public — check them.

- Price growth. Published prices have been rising around 3–4% per year recently, so budget for modest increases; grants don't always grow to match.

- Aid renewal terms. Merit scholarships often require a minimum GPA to keep. Know the renewal conditions before you count the money.

FAQ

Is community college then transfer actually cheaper? Usually much cheaper — two years at ~$4,150 tuition before transferring can cut the total dramatically. The catch is transfer credit: confirm the four-year school's articulation agreement before choosing courses.

Do I have to include housing if I live at home? COA drops substantially for commuters — often $10,000+ per year. Living at home for even part of college is one of the biggest levers a family controls.

Are out-of-state publics ever worth it? Sometimes — several states' flagships offer large merit awards or regional exchange discounts to nonresidents. But full-freight out-of-state ($49,000+ per year) with no aid is one of the hardest prices to justify.

How does this fit into building my list? Affordability is one of the four fits every school has to pass — our guide to building a balanced college list shows where cost fits in, and the class of 2027 financial aid timeline covers when to do each step.

Sources: College Board, Trends in College Pricing and Student Aid 2025; Federal Student Aid, Pell Grant amounts.

Plan your whole college journey with Picka

Search every US college, build a balanced list, map out costs, and stay on top of every deadline — all in one calm, organized place.